Secure Document Sharing

Secure Document Sharing

Investment Basics Series: Bonds vs. Bond Funds

How do I decide whether to invest in individual bonds, bond funds or both?

In our last post, we addressed why we typically advise using stock funds instead of individual stocks to implement your investment strategy. Today, let’s talk about why we usually recommend the same for bonds.

For bond and stock investing alike, turning to low-cost, well-managed funds instead of trying to juggle individual securities is a relatively straightforward way to implement sound investment theory. Simpler logistics and well-managed costs should free you from getting lost in the weeds and help you stay focused on your long-term goals, thus improving your odds for ultimately achieving them.

But, as you may recall from our post about asset classes, stocks and bonds are subject to different factors for explaining their expected higher or lower returns. Factors that seem to drive stock returns include a company’s relative size, and whether it appears to be undervalued or more fairly valued by the market. For bonds, return-driving factors include credit rating and term (i.e., a near or distant due date).

This generates several important differences between stock and bond investing that are worth describing.

Managing risk – In stocks, we employ market risk and its expected returns by tilting toward or away from it depending on individual goals. In bond investing, the evidence has indicated that adding market risk by tilting toward bad credit (“junk bonds”) or going too far out on the term has not offered enough expected reward to justify the added risk. That’s why we typically use bonds for offsetting rather than adding to the risk being taken on the stock side of the portfolio.

Redefining the rules – In stocks, a great deal of the evidence-based action is found in ensuring broad, cost-effective diversification across global asset classes. In bonds, for the reasons described above, the lion’s share of the action is on ensuring that costs and high quality are being well managed. We’re still seeking maximum available returns for the asset class (fixed income), but within a different environment in which “safety first” are the watchwords of the day. This brings us to our next point …

Overcoming opaque trading – In publicly traded stock markets, current pricing is readily and freely available to individual investors. In the bond markets, not so much. Bond trades are often subject to burdensome broker markup and markdown fees that are far from transparent. Fair pricing on infrequently traded bonds may be difficult to determine. Bonds also can be fraught with hidden “gotchas” such as underlying vs. published ratings, early call dates, and minimum investment requirements that range in the tens of thousands of dollars per bond.

Suffice it to say that making the most of your bond investing requires every bit as much careful scrutiny, but the information necessary to perform this due diligence is difficult at best for individual investors to obtain. For better or worse, this creates an environment in which professional fund managers with greater access to the necessary details can both simplify your efforts and negotiate on your behalf to maintain minimal costs and quality yields.

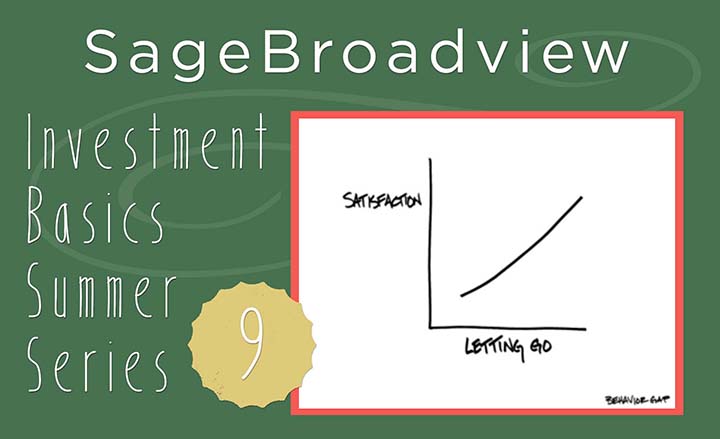

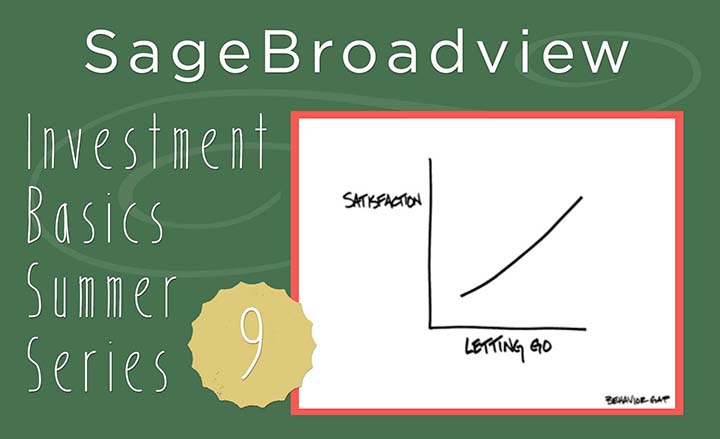

As we concluded for stocks versus stock funds, by ensuring that a bond fund manager’s fees are modest, and that its team is fully committed to the same, evidence-based investment principles we’ve been describing, you can likely let go of selecting individual bonds and redirect the time saved on enjoying a satisfying lifestyle, this summer and year-round.

Win a copy of Carl Richards’ new book, One-Page Financial Plan

As we mentioned in our Investment Basics introduction, send us an e-mail with a question or comment about today’s post, and you’ll be entered to win this week’s drawing for a copy of Carl Richards’ One Page Financial Plan. Happy summer reading!

Sage Serendipity: Neurologist and best-selling author Oliver Sacks (The Man Who Mistook His Wife for a Hat, Awakenings) died this week. It was just this February when he announced his fatal diagnosis in an op-ed article in the New York Times. One of the best ways to learn about Dr. Sacks is to listen to him talk. Radiolab, the radio program and podcast related to science and storytelling has been featuring Dr. Sacks since they began in 2007. Here is a collection of their interviews.

Sage Serendipity: Neurologist and best-selling author Oliver Sacks (The Man Who Mistook His Wife for a Hat, Awakenings) died this week. It was just this February when he announced his fatal diagnosis in an op-ed article in the New York Times. One of the best ways to learn about Dr. Sacks is to listen to him talk. Radiolab, the radio program and podcast related to science and storytelling has been featuring Dr. Sacks since they began in 2007. Here is a collection of their interviews.